Athenian retailers may not have gone skipping and laughing to the bank at Christmas, but supermarket owners catering for our stomachs had more satisfied looks than some.

The purses of Athenian shoppers may be stuffed – if not with the “shoddy silver-plated coppers” Aristophanes poured scorn on in 405 BC – then certainly with the most inflated currency in the EC. For what it is worth, though, about 60 percent of the money spent on consumer goods goes to supermarkets.

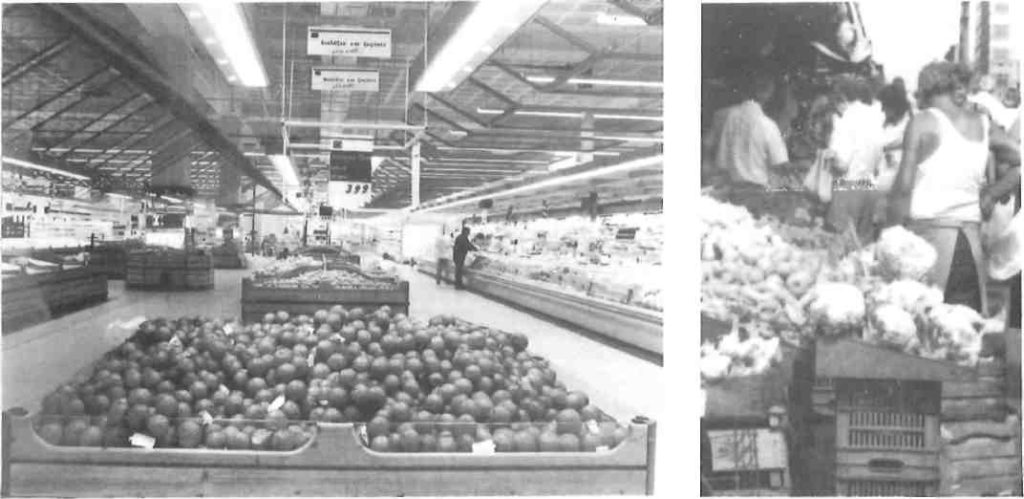

In the last 30 years Athens has seen some of the most intensive supermarket development in Europe. By the end of the 1980s, Attica had one supermarket for every 8200 inhabitants, even more than (then West) Germany with one for every 8266. (France is still better off, one for every 8000, followed by Denmark, one for 6875, then Belgium, one for 5000).

“Greek supermarkets have been experiencing continuous increase, approximately 7 percent annually, and in urban areas the increase has reached saturation point,” says Dimitris Michailidis, spokesman for the Greek Supermarket Owners’ Association.

He has statistics showing growth from 428 in 1978 to 448 in 1980, 635 by 1987,996 by 1989. The obverse of these figures is that in the same period 6000 Greek grocery shops closed and in the decade before, 1969-78, as the first 4000 or so supermarkets sprang up, 7000 other groceries had disappeared. While supermarket turnover share rose to 60 percent of food store turnover, small groceries’ share fell from 30 to 20 percent, though big groceries’ share remained about static at 20 percent.

Supermarket chains, too, increased in number from 32 in 1982 to 72 in 1990, but only a dozen chains had more than 16 outlets, with six others having 11 to 15, 22 six to ten and 32 only three to five.

The Marinopoulos family pioneered Greek supermarketing, opening the capital’s first self-service store in 1961, a 20-square-metre outlet in Kolonaki, two others the following year, and then burst forth as Prisunic Marinopoulos in Leoforos Alexandras in 1965. The 25th company supermarket opened at Veria, west of Thessaloniki at the end of last year, and Prisunic Marinopoulos has become the giant of Greek retailing. It has also been granted the important Marks & Spencer franchise. Including turnover from the Tresko chain of 15 stores acquired in 1990 for over two billion drachmas, supermarket sales totalled 54 billion drachmas in 1990.

The Sklavenitis chain followed with 1990 sales of 35.66 billion drachmas, then Hellaspar Veropoulos with sales of 26.6 billion. Ranking fourth in terms of turnover was Alpha Beta Vassilopoulos with sales of just under 20 billion.

The market leaders keep on growing. Sklavenitis opened its 25th outlet in Attiki last June, a 2000-square-metre store, and Hellaspar Veropoulos its 40th, also 2000-sq-m., in Kato Kifissia in May. Most conspicuously, Vassilo-poulos opened Mega Alpha Beta, its 16th outlet, Greece’s biggest supermarket up to that time, 10,000-sq-m. including selling space and warehousing, near the airport.

The new Mega Alpha Beta raised Vassilopoulos turnover 140 percent initially, says Gerasimos Vassilopoulos. Sales one summer week reached nearly 183,000 million drachmas. He was not surprised, having anticipated good business on Leoforos Vouliagmenis near the airport, with 35,000 vehicles passing daily.

Others in the trade watched amazed, believing the area was well enough served with supermarkets. The Prisunic Marinopoulos outlets at Alimos, Neo Phaleron and Glyfada suffered, but by the autumn reports suggested established outlets were regaining old patronage.

“Supermarkets are still in an expansionist phase,” says George Meimarides, President of the Greek Retailers’ Association. “But even they are feeling the pinch. There has been a drop in GNP, with nil, possibly negative growth, and a credit squeeze, with interest rates up to 35 percent. The government stabilization program has reduced private demand, even if it has not managed to curtail the public sector, so the overall pie has shrunk. The public sector’s slice is bigger, and the private sector slice has contracted violently’.

In this setting, Greece’s first foreign hypermarket opened on 5 November, the 7000-sq-m. Continent in Alimos, with parking for 1000 cars, run by the French hypermarket giant, Promodes, keen to expand in southeast Europe after joint-ventures in Germany and Portugal and acquisitions in Spain.

Promodes is the fourth largest retail enterprise in France with a turnover in 1990 of 58.5 billion French francs, following Leclerc with sales of 100 billion French francs, Intermarche with sales of 96 billion and Carrefour with sales of 76 billion.

A second Continent is planned for Thessaloniki, says the Promodes office in Athens. Pricing benefits from bulk-buying and experience in setting up technologically sophisticated supply channels. Traditional Greek are likely to feel seriously challenged as the year goes on.

Take fish: Portuguese fishermen on the’Atlantic coast used to supply coastal town and village fish markets. Their catches now go to icy collection centres where an all-seeing computer eye sorts crabs from prawns, cod from cuttlefish in split seconds. Hypermarkets buy mega loads and work on 1 percent profit margins. Traditional operation cannot compete.

A feature of supermarkets like Prisunic Marinopoulos and Vassilopoulos is their diversification into extensive non-food sections offering household goods. Some of these areas will be affected by competition from the other newcomer late last year in Alimos, Praktiker Hellas.

The 5000-sq-m. outlet on the corner of Alimou and Leoforos Vouliagmenis, with a 2000-sq-m. garden centre over the road and parking for 500 vehicles, is generally a technical department or do-it-yourself store. Praktiker carries all a home-owner needs from fittings and fixtures, flooring and carpet, ready-made and kit-set furniture, a customer design service, household equipment and appliances.

Prices are extremely competitive, quality guaranteed. Praktiker has scores of suppliers, many Greek, some German who already provide merchandise for the 97 outlets in Germany. Local suppliers required to specialize to meet Praktiker standards are learning new skills and will attain higher levels of expertise.

While a new enterprise, the company is only half foreign. Shelman, Greece’s top wood manufacturer, is a 50 percent partner in the joint venture with the powerful Asko Deutsche Kaufhaus. The agreement was finalized two years ago, after Shelman dropped negotiations with Promodes.

The Greek company has been looking for a foreign partner to embark on a major retail enterprise for the last 10 years or so. Building has already begun on the second Praktiker, twice the size of the first, on Pireos and a third outlet is mooted for Athens, possibly on Leoforos Kifissias. Expansion is to be financed by profits which will remain in Greece for the first five years. Land purchase is being made with three billion drachmas from the German partner.

Set up 30 years ago, Shelman is an importer of mainly tropical timber from Africa through its own port. Logs are processed for both the domestic and foreign markets. Products range from ordinary sawn timber of species including sapelli, tiama, khaya, iroko, Iimba, ayous, sipo at an up-to-date mill, to plywood veneers, using Japanese technology, a wide range of parquet flooring, blockboard and chipboard for carpentry and furniture, plywoods for exterior and marine use, furniture and concrete shuttering.

Shelman reported sales of 19,453 billion drachmas in 1990 and profit after tax of 1,586 billion. Exhibition centres have been opened in Maroussi and Thessaloniki for private customers and contractors and others are planned. Participation in the joint venture with Asko involves one of the largest investments in Greece, according to the 1990 company annual report.

Asko is a rapidly expanding German retailer with origins in the cooperative movement. Company strategy till recently was to open hyper-markets on cheaper land on city fringes. Like other major German retailers such as Spar, Tengelmann and Edeka, Asko’s chief effort is directed at expanding in former East Germany with a planned chain of 70 outlets.

The company is expeced to be taking over eight Continent hypermarkets which it has been running as a joint venture with Promodes. Other Asko interests are a joint venture with the Bulgarian department store group, Denica, expansion to be financed from profits over the next five years.

Although the EC will be a single market a year from now, major retail operations remain distinctly national. Shopping preferences tend to be highly localized. Southern European countries, especially Spain and Portugal, to a lesser extent Greece, prefer buying local goods, above all when it comes to food, so the provisional results of an EC survey show.

For this reason, franchise operations run by locals sensitive to local taste, traditions and ways of behavior, are favored as a method of expansion, rather than acquisitions or joint ventures. Franchising is well developed in Spain and Portugal and, at least in fashion, in Italy. In Greece it is developing. The Europeanization of Athenian retailing is apparent: Benetton and the Body Shop, Marks & Spencer and Mothercare elbow each other in the more chic streets.

Greece has been familiar with the Marinopoulos French connection since 1965, but the Prisunic input has been important know-how put at Marinopoulos disposal. Vassilopoulos has several foreign liaisons, with the second largest Belgian retail enterprise, Delhaize Le Lion chain, which markets Greek fruit and vegetables; with the Italian Ipercoop, which provides data processing know-how; with the Swiss Globus group, for reciprocal promotions. But heavy-weight foreign retailing began only late last year.

Greece has been late in seeing foreign restaurant chains take up prime public space. Home-grown Goody’s has had the fast food market to itself for 15 years while opening 55 outlets, 22 in Athens.

Only at the end of last year did McDonald’s arrive with food technologist George Yiakos, the franchise-holder. It will open a second outlet in Piraeus this year. Pizza Hut, a Pepsico-owned sister of Kentucky Fried Chicken, opened two outlets in 1990 and plans several others. The franchise-holder is John Exharchos. The smaller Wendy’s had three outlets doing lively business in Athens by the beginning of the winter, with franchise-holder Nikas, the salami and sausage producer.

Price controls covering eating places using disposable dishes, cups and cutlery, rather than passionate attachment to souvlakia, were the reason for McDonald’s tardiness, according to Meimarides. By Greek government decree, restaurant offerings on paper plates to be eaten with plastic cutlery by diners seated on stools or benches rather than straight-backed chairs could not be priced above a certain level. “As the outlets were in lower restaurant categories, McDonald’s could not charge enough to put good meat in their hamburgers,” he said.

After the 1990 easing of price controls, the way was clear for Big Macs and, an innovation for the Greek gas-tronome, cod-filled sandwiches with tartare sauce and feta.

Yiakos has given assurances international McDonald’s standards will be kept up in Syntagma Square. The only Greek products on the menu will be Coca-Cola and a new variety of lettuce specially grown locally for the company. All else from meat, bread, potatoes and dairy products (including presumably the feta) to paper plates, cups, napkins and super-thin straws will come from Germany. If or when Greek producers are big enough and suffi-ciently well organized, McDonald’s would switch to local suppliers.

McDonald’s debut in Athens is a rare example of major retail development under the worst of the nefos. “Retail business has fallen 50 percent in central Athens in the last ten years,” says Meimarides. “The single main cause has been the curtailment of private cars by the introduction of odd and even number plate days in 1983. The big slump began when this law was first applied from 8am till 4pm, and then extended till 8pm in 1987.”

Arson attacks by the November 17 terrorist group on the main department stores, targeted as concentrations of capital, in the late 1970s also cast a blight. One store collapsed, never to rise again. Minion, uninsured, was taken over by the government to protect about 800 jobs.

Lambropoulos, Athens’ biggest and oldest department store, denies trade fall has been as much as 50 percent. Store manager Varvara Fantoussi-Travassarou says emphasis on first-class service, new displays and in-shop boutiques helps keep customer loyalty among important groups like the foreign community and embassy staff. The company is following with the suburban expansion trend by opening a 1000-sq-m. Glyfada boutique and further expansion will be in the suburbs.

Lambropoulos became a public company 20 years ago, and though two Lambropoulos brothers still have about 10 percent of shares and one is managing director, shipowner Eftathios Gourdomichalis has a large, though not maj ority, shareholding and is vice-chairman.

Minion reverted last year to its founder-owner, John Georgakas, an energetic 78-year-old with memories of Athenian retail trade back to his pre-war days running a periptero near Omonia Square. The government has subsidized the store to the tune of 400 billion drachmas, he says, but the balance of 2.4 billion required came last September from two friends, shipowner Nikos Vernikos and Takis Isaiadis, the Sharp agent in Greece.

“I believe in department stores,” says Georgakas. “I’m ready to fight. Athens has a population of four million. Another four million Greeks visit each year from the provinces. About five million tourists visit Athens each year and half come through Minion. I’m sure there’s a future for us.”

He plans to float Minion on the Athens stock exchange “when prices have risen” in several years. A franchise outlet is planned for Thessaloniki. “There’s a big market there and rich surroundings. The city will grow in importance as a Balkan port. Thessaloniki is a must.”

Athens’ third department store, Klaoudatos, rising above the central market, also concentrates expansion away from the capital city. A new 7000-sq-m. outlet was ready to open in Agrinion, in western mainland Greece, at the end of last year. A branch began in Larissa in 1990 and a chain of sports goods shops is planned. Negotiations to become a franchise partner with British Home Stores have been reported.

In spite of mega operations, the demise of the small shopkeeper still seems a long way off in Greece. The country had more shops per person than anywhere else in Europe, 18 shops for every 1000 Greeks, an EC survey showed in the mid-80s. (Italy was next with 15, France 12, the Netherlands 11, Denmark nine, Germany and Britain six).

Greek shops were small businesses though, with only 1.6 employees each, followed by Italian shops with 2.2, Dutch 2.9, Danish 3.6, French 4.6, German and British six.

A National Statistical Service of Greece survey showed Greece had 215,000 shops by the end of the 1980s, more than double the number 30 years before. But the 1000 supermarkets among them enjoyed 60 percent of the takings.

Nielsen Hellas which does these surveys no doubt knows its onions and can identify a shop when it sees one. Is a periptero a shop? Is the hole-in-the-wall egg merchant, who sells rotten fruit on the side to the queue of sick and maimed in the street market a shop? Is MY egg-seller, who asks what I’ll do with two eggs and what’s going in the omelette a proper retailer? And what about the garlic ladies and camomile and mountain tea men and a plethora of sellers of collectibles and souvenirs in the Monastiraki market, which differs in little but language-from a Turkish bazaar or Arab souk? Are they counted as retailers for the .Single European Market data bank in Brussels?

The Breton garlic brigade with their berets and bicycles could be threatening the livelihood of the voluminous-skirted garlic ladies of Sofokleous by the turn of the century. They may need tagging as an endangered species.